Single-home buyers and condo living on the rise; here’s what you need to earn in Hamilton-Burlington

Published February 12, 2020 at 4:42 pm

Despite two incomes being better than one when it comes to real estate, single-person households have become the most common type in Canada for the first time in our nation’s history.

Despite two incomes being better than one when it comes to real estate, single-person households have become the most common type in Canada for the first time in our nation’s history. The latest census data reveals the number of people living alone has doubled from 1.7 million in 1981 to four million in 2016. In fact, single ownership rates are now 50% – up from 32% in the ‘80s – with one in five live in a condo apartment.

Not surprising, as apartment living offers amenities that are ideal for many single lifestyles such as a lower price point and smaller living space, with maintenance and repairs covered by a condo board.

So if you’re single and looking (for a condo), where should you go?

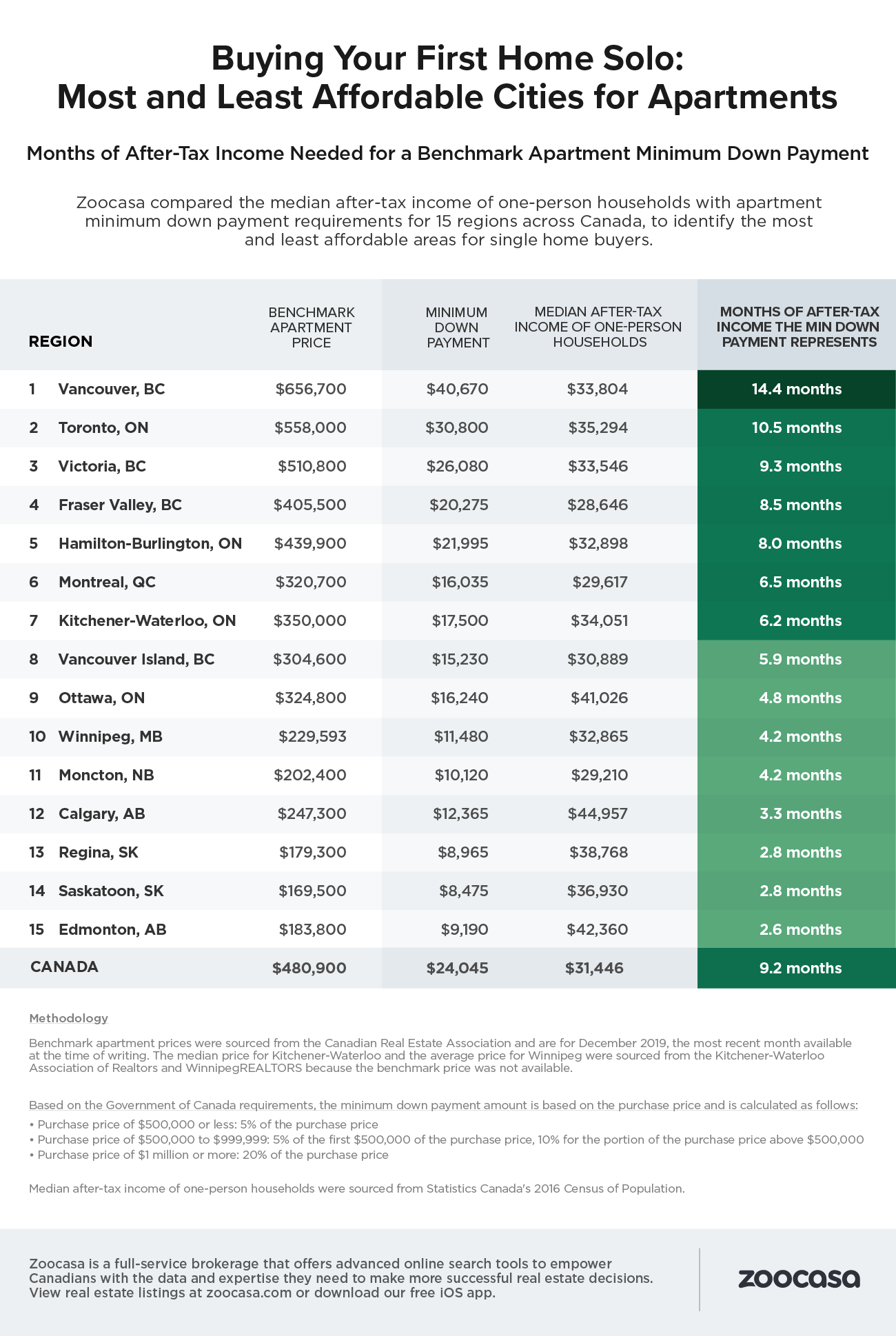

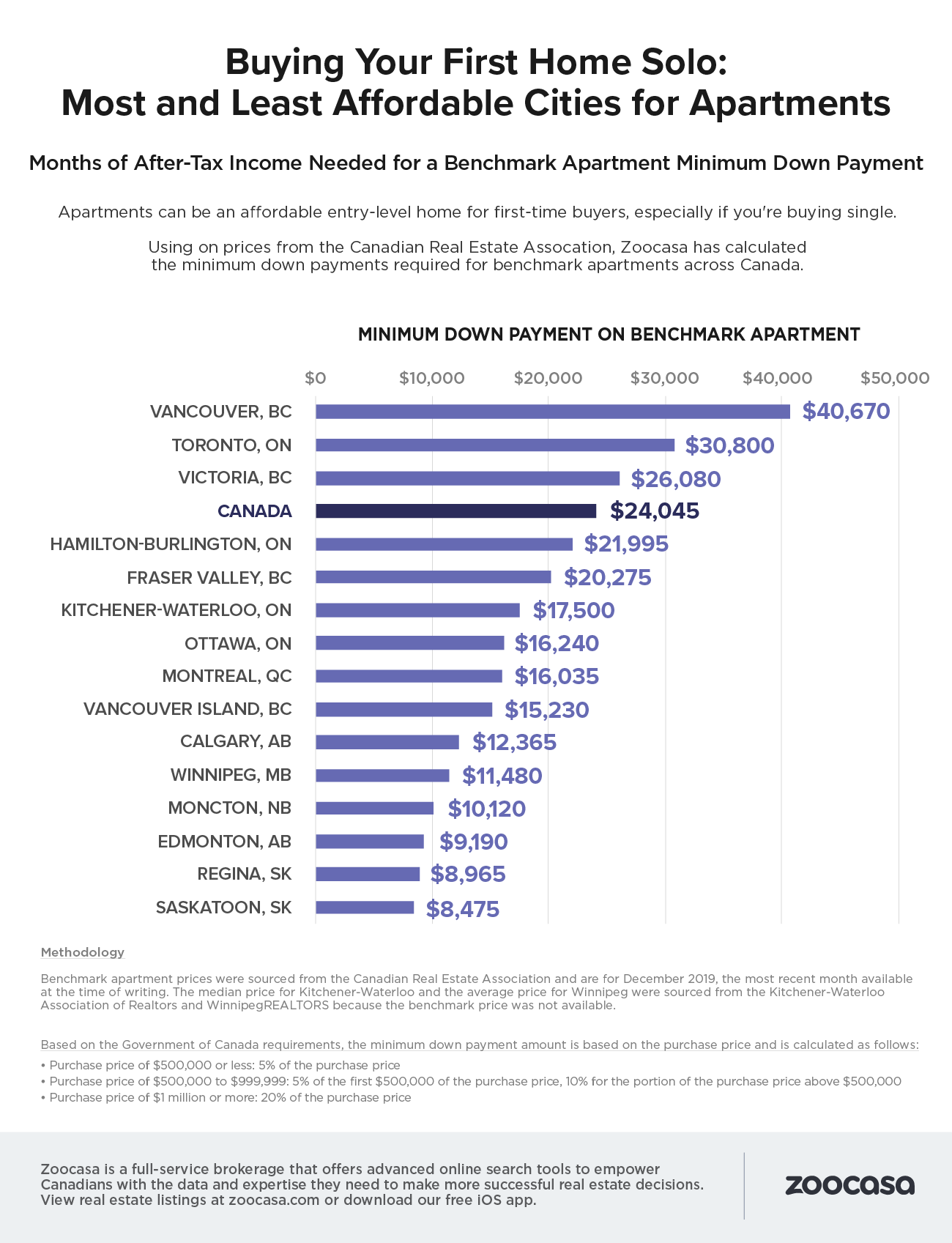

Zoocasa crunched the minimum down payment needed to purchase a benchmark condo or apartment and compared it to the after-tax single-household median incomes earned in each. The study also calculated how many months it would take for such a home buyer to save up the necessary down payment, assuming they could contribute 100% of their income annually.

Hamilton-Burlington came in fifth. According to Zoocasa, 8 months of after-tax median income would be required to afford a minimum down payment of $21,995 on a benchmark $439,900 mortgage. Which means you would likely need to earn $32,898 in year after-tax income.

Videos

Not surprisingly, the numbers reveal it is toughest to purchase a home on a solo budget in Canada’s biggest cities. For example, to purchase Vancouver real estate, which has long held the distinction as the nation’s most expensive, the required down payment would be greater than what is earned by a median single-income household in an entire year.

There, a benchmark apartment costs $656,700, requiring a minimum down payment of $40,670, outstripping the $33,804 earned by single buyers. Should that individual set aside their entire earnings to save for a down payment, it would take them 14.4 months to pull together the needed cash.

Affordability is less steep, though still challenging, for homes for sale in Toronto; there, a benchmark apartment of $558,000 would require a down payment of $30,800, just shy of the median income of $35,294, requiring a 10.5-month savings timeline.

As has been the long-term trend, single buyers seeking the greatest bang for their buck will find it in the Prairies; in the three most affordable cities, a benchmark apartment can be purchased for under $200,000, with required down payments making up a comparatively smaller portion of incomes.

insauga's Editorial Standards and Policies advertising